Table of Contents

Lengthy, error-prone financial reporting processes are quickly becoming a thing of the past. As we lean more on data than ever before, finance professionals are ditching inefficient manual processes to leverage financial reporting automation. What is automated financial reporting? It’s the process of using software to automate the tasks involved with generating financial reports. The software can automate data collection, processing, and analysis, enabling professionals to quickly extract data-informed insights. But why automate financial reporting? The answer is simple. If you want to track financial performance, maintain financial stability, and identify profitable opportunities, you need accurate, reliable financial reports—and you need them quickly. Financial reporting automation reduces errors, increases data quality, and delivers data to your fingertips at speed. But as with all automation initiatives, there are considerations to be aware of if you want to maximize results. We’ve compiled seven best practices to help guide you through your financial reporting automation journey.

» 7 Best practices to maximize financial reporting automation

1. Select the Correct Financial Reporting Software

Searching for the right financial reporting software can be daunting. It’s important to consider your business’s goals and needs as you wade through the options, as it may require you to choose particular types of software. Let’s go over the different types of financial reporting software available.

Types of financial reporting software

-

- Accounting software

Accounting software performs several key functions that aid financial reporting automation—for example, automated invoice generation, bank reconciliation, receipt capture, and data entry. Not only does this reduce error, improve accuracy, and save time, but the best accounting solutions also generate advanced, customizable reports for easy analysis.

-

- Business intelligence (BI) tools:

BI tools use data visualizations, such as pie charts and graphs, to transform convoluted financial data into easily interpretable financial reports. This increases the accessibility of data for finance teams and stakeholders alike, enabling the quick identification of patterns and trends.

-

- Enterprise Resource Planning (ERP) software

ERP software increases the efficiency and effectiveness of financial reporting automation by integrating your financial reporting with other business applications. Financial data from every corner of your business—marketing, HR, inventory management, etc.—can be centralized into a single system for a holistic view of your business’s financial health.

-

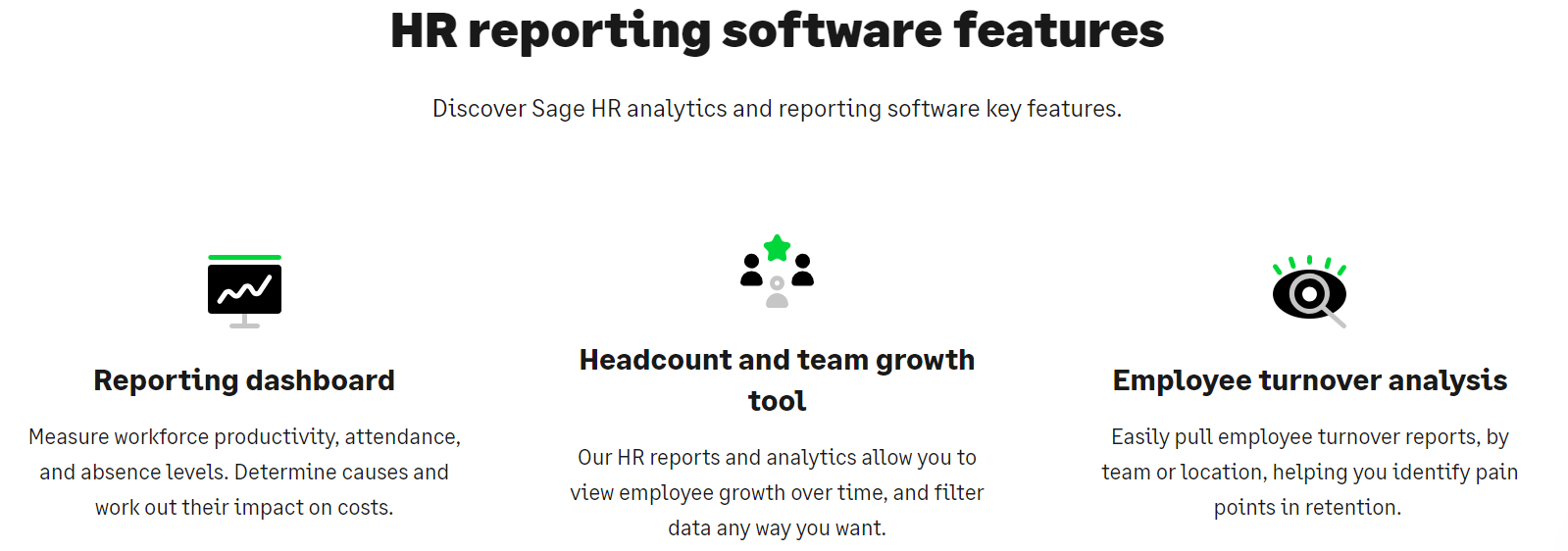

- Expense management software

Usually offered by an HR reporting software provider, expense management software automates expense recording by letting you submit and track expense entries online in real-time. This information is then fed into financial reports. HR reporting software also lets you measure attendance, absences, and productivity to accurately determine their financial impact.

Screenshot taken from sage.com

It’s not just the type of software you need to consider, but the features that they offer, too. Here are the main ones to keep in mind.

Features to look for in financial reporting software

-

- User-friendly reports

If your chosen software’s reporting structure has a steep learning curve or lacks customizability, it will slow down productivity. The financial reports produced by the software should display data clearly and accurately. They should also feature customizable dashboards and reports. At a glance, your team should be able to access and interpret the metrics that matter most to them.

-

- Intuitive interface

In the same vein, your chosen software should be easy for your team to navigate. To accommodate varying levels of tech-savviness within your team, aim to balance functionality and features with intuitive controls. This is so that everyone using the software can extract the same degree of value from it.

-

- Actionable insights

Your finance team should be able to extract actionable insights from the advanced analytics presented by your software. These insights can illuminate trends and patterns, and power pivotal, forward-thinking decisions.

-

- Cloud-nativity

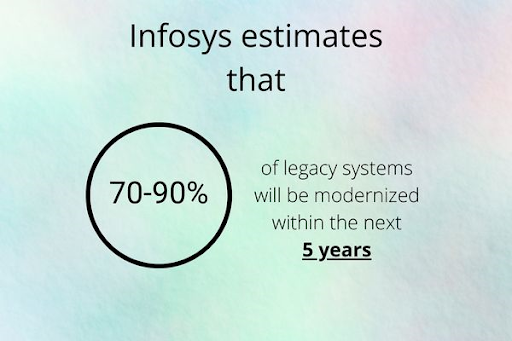

A financial reporting solution built with native cloud architecture delivers the scalability, flexibility, and centralization that on-premises solutions lack. You can benefit from regular, automated updates to make sure your solution is secure and bug-free. According to Infosys, cloud benefits are a key reason why an estimated 70-90% of legacy applications will be modernized within the next 5 years.

Image created by writer Data sourced from infosys.com

2. Implement Proper Data Integration and Data Quality

Applications that exist in silos will generate data in silos. Siloed data (i.e., datasets that exist at department-level on independent systems) harms financial reporting by creating inconsistencies. When teams must manually collect, update, and share datasets, the risk of error is high. Plus, financial reports take longer to produce, significantly limiting real-time decision-making. These difficulties have far-reaching financial consequences. For example, if your marketing department doesn’t have access to updated financial data, they might overestimate marketing budgets. If sales don’t have access to marketing and accounting data, it can skew pricing strategies and result in financial loss. And, of course, serious issues arise when accounting can’t access every department’s financial data. Lack of accurate, real-time, and complete data visibility can skew cash flow forecasts, impair resource allocation, and lead to other critical failures in judgment that negatively impact financial performance. Data integration means taking data from various sources and combining it into one unified system. This is typically achieved using powerful ERP software solutions. When you integrate your financial reporting software with your other accounting systems, you eliminate silos and provide your business with a single source of truth for financial data. There are many benefits to this. Data integration:

-

- Enables the automated collection, processing, and reporting of data.

- Increases data quality by reducing manual data entry.

- Enriches data visibility to drive insights into the relationship between financial data and other data, such as inventory, sales, and HR.

- Improves collaboration between departments, driving unified decision-making.

3. Standardize the Whole Reporting Process

Standardizing financial reporting involves devising a clear reporting process that is followed by every department in your business. A standardized process guarantees that your data is accurate and consistent, and helps generate valuable insights. Plus, it streamlines internal workflows and collaborative efficiency. But there’s another critical reason why you should standardize your financial reporting process. To comply with the Generally Accepted Accounting Principles (GAAP), you need to follow the principle of consistency. The principle of consistency is one of many principles outlined in the GAAP. It dictates that methods and processes of financial reporting should stay the same to deliver financial comparability between different business time periods. To remain compliant with GAAP and avoid financial penalties, make sure you use a standardized financial reporting process. How do you do this? Standardized financial reporting typically involves devising a collection of policies, methods, and structures such as:

-

- Standardizing formats for data such as dates, currencies, and card details to provide uniformity across departmental data sets.

- Using automation tools where possible to automate data entry in consistent formats and reduce the risk of inputting errors.

- Using standardized templates and presentation styles for financial reports to aid swift interpretation and comparison of data.

- Making use of data visualization tools to improve data accessibility and interpretation for teams and stakeholders.

4. Automate Your Data Collection

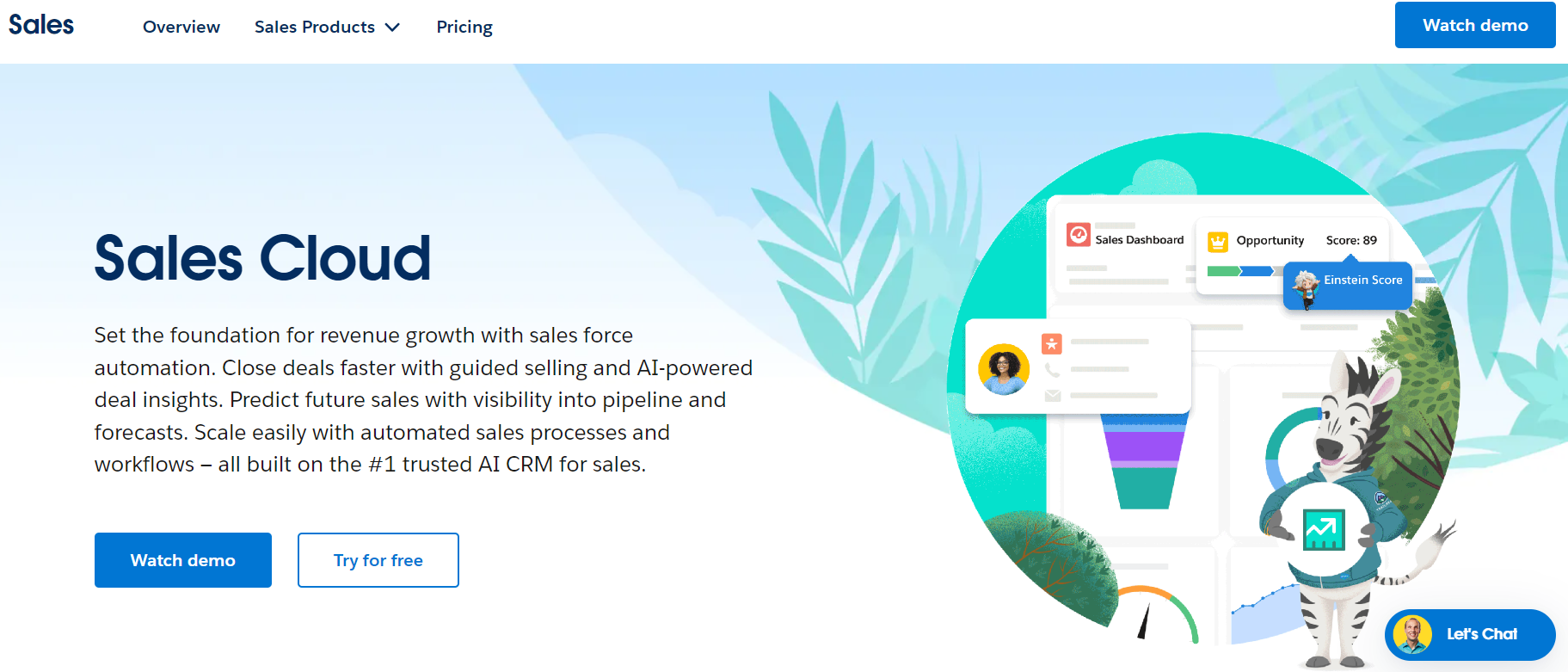

The manual data entry process is inherently flawed. It’s tedious and time-consuming for employees and can lead to data being mistyped or not completed in full. Plus, if data formats haven’t been standardized across departments, data duplication and other formatting issues can erode data quality and lead to inaccurate insights. Automating data collection involves using digital, machine-learning technologies to capture data from various sources and pool it into one central repository without human intervention. Unlike human employees, AI technologies digitize vast volumes of electronic and paper documents in seconds. They don’t get tired, bored, or distracted, making them the perfect resource to handle repetitive labor. This leaves your employees free to tackle more complex, satisfying tasks. Take Human Resources, for example. Instead of wasting productivity on data entry, HR teams can automate data entry for payroll, expenses, and other people processes using online HR software. This gives them more time to perform employee-facing activities. Another benefit to automated data collection is that it speeds up your financial reporting process. Let’s say you use a CRM such as Salesforce to automate data entry. When integrated with an accounting system, your CRM can automatically send customer data to finance and accounting without having to request it from marketing. Revenue can swiftly be traced back to specific marketing campaigns without the stress of human error skewing analysis.

Screenshot taken from salesforce.com

5. Implement Strict Security Measures

Data security should remain a top priority as you implement financial reporting automation. All data, whether it exists in the cloud or on-premises, is vulnerable to threats at rest and in transit. Keeping your data secure will protect you from security risks and keep you compliant with GDPR, CCPA, and other regulatory legislation. Along with investing in cybersecurity software, what other security measures should you implement?

-

- Data encryption

Sensitive data should be encrypted so that it can only be read by authorized personnel. Data encryption turns human-readable plaintext into unintelligible ciphertext, making it significantly harder for hackers to interpret it.

-

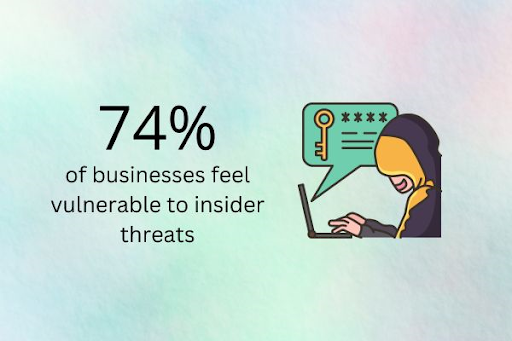

- Access controls and permissions

Beware insider attacks. 74% of businesses feel vulnerable to insider threats. Privileged IT users and admins are deemed to pose the biggest risk, followed closely by other privileged business users and executives.

Privileged account misuse can lead to data breaches and fraud. So, it’s vital that you put restrictive measures in place to prevent unauthorized access and misuse. You can do this by establishing and enforcing access permissions for systems, accounts, and specific data sets. Make sure that users only have access to the systems and data that are necessary for their role. Don’t forget to use multi-factor authentication and revoke access upon an employee’s departure.

-

- Data security awareness training

Your employees are one of the first lines of defense against cybersecurity attacks. Creating a data security awareness course can help them protect your company, customers, and themselves. Some topics that you should cover include:

-

- Practicing good password hygiene.

- Spotting suspicious emails.

- Using a VPN to access company networks and view sensitive information.

- Identifying social engineering attacks.

- Following the right incident response protocols.

6. Run Automation Reviews and Audits

By conducting regular automation audits and reviews, you can verify data integrity and make adjustments based on the results of your analysis. As a best practice, use audit management software to automate your audit schedule and access detailed feedback. During your audit, evaluate the efficiency of your reporting process in comparison to your manual processes. This will help you establish whether your automation operations are successfully streamlining workflows and enhancing productivity. Do the same comparison with data quality. Determine whether the quality of your data—and the results extracted from this data—meets your goals and expectations.

7. Nurture User Training and Support

So, you’ve implemented fancy new accounting, BI, and expense management tools to automate financial reporting. But if your employees don’t know how to use these technologies, leveraging automation to its full potential will be impossible. Remember, automation is only as good as the talent operating it. So, invest in training to help your team use technologies and tools properly. The way you decide to do this is completely up to you. Ask employees how they’d prefer to learn, whether it be through classroom-based learning or a series of online courses via a learning management system. You can even approach your software provider. Most providers offer tutorials, live support, and online knowledge bases.

» Final Thoughts

Financial reporting automation is the future for businesses wanting to extract actionable insights from hyper-accurate, reliable financial data. Instead of channeling their productivity into mundane data entry tasks, finance professionals can concentrate on analysis, forecasting, and other transformative business activities. But instead of rushing into it, follow best practices to maximize the success of your automation initiatives. Select the right tools, integrate your systems, automate data collection, and standardize the entire process to remain compliant.